Are You Sure Your Next Payment Is Going to the Right Account?

Every day, businesses across Europe send payments to suppliers, partners, employees, and customers — trusting that the account details they have on file are accurate and legitimate. Most of the time, they are. But when they aren’t, the consequences are swift, costly, and hard to reverse.

Verification of Payee (VoP) exists to close that gap. If you’re processing payments, keep reading to find out how to prevent fraud before “it’s too late to apologize”.

What Is Verification of Payee and How Does It Work?

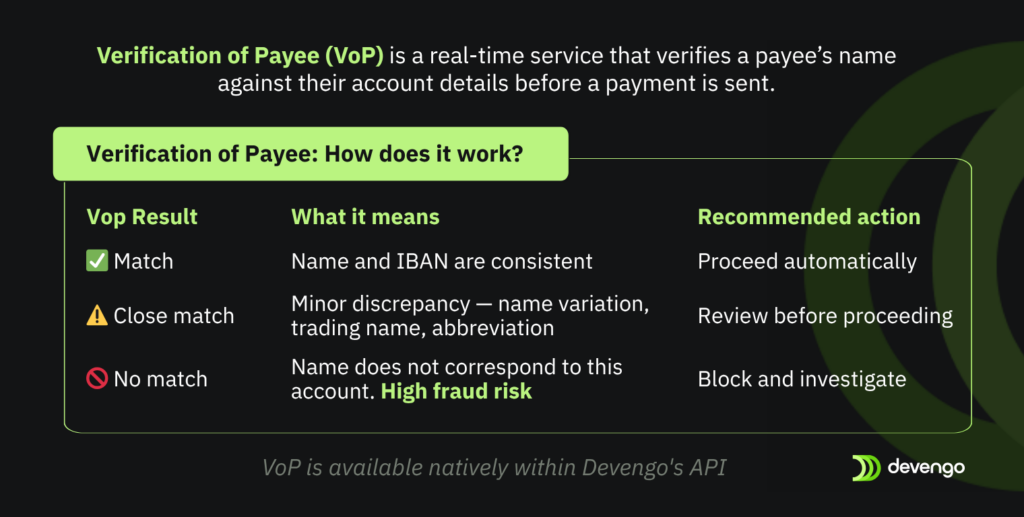

Verification of Payee (VoP) is a real-time bank account verification mechanism mandated under the EU Instant Payments Regulation (Regulation EU 2024/886) with mandatory compliance from 9 October 2025 for instant credit transfers. It requires payment service providers to confirm the alignment between the payee’s name and IBAN before executing a credit transfer — not after, not in a batch review, but in real time, before funds move.

A fraudulently substituted account fails immediately. An honest error surfaces before any money moves. In both cases, the check happens before it’s too late to act.

The Risk You’re Carrying With Every Unverified Payment

The most common type of payment fraud in Europe doesn’t rely on complex hacking techniques. Instead, it targets a simple weakness: communication.

Fraudsters intercept a supplier email, an invoice, or an onboarding form — and swap the legitimate bank account for their own. Your team approves the payment. The transfer goes through. The money is gone.

This is business email compromise (BEC) fraud — one of the most common forms of authorized push payment (APP) fraud, where victims are manipulated into sending money themselves rather than having it stolen directly. According to the European Banking Authority, this type of fraud accounted for 57% of total credit transfer fraud value in Europe in H1 2023.

What makes it so effective is its simplicity: the payment is legitimate in every respect except the destination account. Standard controls don’t detect it and by the time the error surfaces, the receiving account is already empty.

The common thread: all of it happens after the payment has already been sent. At that point, your options are limited.

What makes credit transfer fraud particularly brutal from a legal standpoint is that recovery is rarely guaranteed. Once the funds are gone, you’re in a long, uncertain process. VoP is simply one of the best secure insurance you can get — and it works in real time.

Want a deeper dive into VoP for EU companies? Read our full guide.

Why VoP Changes the Equation

VoP moves the check to before the payment executes. Before funds leave your account, VoP queries the destination bank in real time and confirms whether the account name you have matches the actual account holder.

You’re not adding friction to every transaction. You’re making sure the rare cases that actually need attention — the ones that would otherwise cost you — get caught before they do.

The Business Case Is Simple

The operational cost of investigating a single misdirected payment — finance team hours, back-and-forth with banks, potential legal escalation — is entirely avoidable. VoP catches the error before the payment executes. No investigation needed, because the problem never happens.

Every payment that returns a no match is a misdirected transfer and a potential recovery process avoided. Every close match is a discrepancy caught before it becomes a problem. The check takes milliseconds; the alternative can take months.

VoP integrates directly into your payment flow via API. Once it’s in place, every transfer is checked automatically, in real time, before funds move. No added friction, no operational overhead.

Protect your transfers with Devengo

Devengo is a regulated payment institution, supervised by the Bank of Spain and authorized to operate across the European Economic Area.

Verification of Payee (VoP) is natively available through Devengo’s API, built on SEPA Instant infrastructure. No additional vendors. No compliance overhead. No new contracts.

We also offer account verification solutions across Spain and SEPA to reduce fraud risk and increase payment certainty.

Are you a bank or PSP? → Explore Verification of Payee for SEPA.

Not a financial institution? → Talk to our experts to explore the right verification setup for your business.